The Market Mindset: how Canadian households split, share, and hide their finances

June 4, 2026

.png)

Canadians are facing unique financial headwinds — sky-high housing prices, economic uncertainty, and technological disruption. As a result, we are seeing retail investors become more resourceful than ever. They are increasingly confident, engaged, and willing to take control of their financial futures. The Market Mindset is a series exploring how Canadians think about the present and future of investing.

You can learn a lot about a household by how it manages its finances. Money is at the centre of all modern relationships, and not just because it pays the bills, buys a night out, or secures a well-earned retirement. Disagreements over money are among the most common reasons couples split up. And, right now, Canadians are facing some serious financial pressures.

We wanted to better understand how couples think about and manage their finances together. We surveyed 1,742 Wealthsimple clients in April — a mix of singles, common-law and married couples, parents, and multigenerational families.

Here’s what we found:

Financial infidelity is more common than you’d think

Most couples expect to manage their money as a team, especially if they move in together or have children. Financial infidelity, or the act of keeping financial secrets from one's partner, turns out to be a lot more common than we expected.

About 14% of couples we spoke to admitted to financial infidelity, while another 1 in 5 confessed to downplaying or minimizing a purchase when talking to their household. What they hide is rarely headline-grabbing — much of the friction in Canadian households lives in everyday decisions, not big purchases.

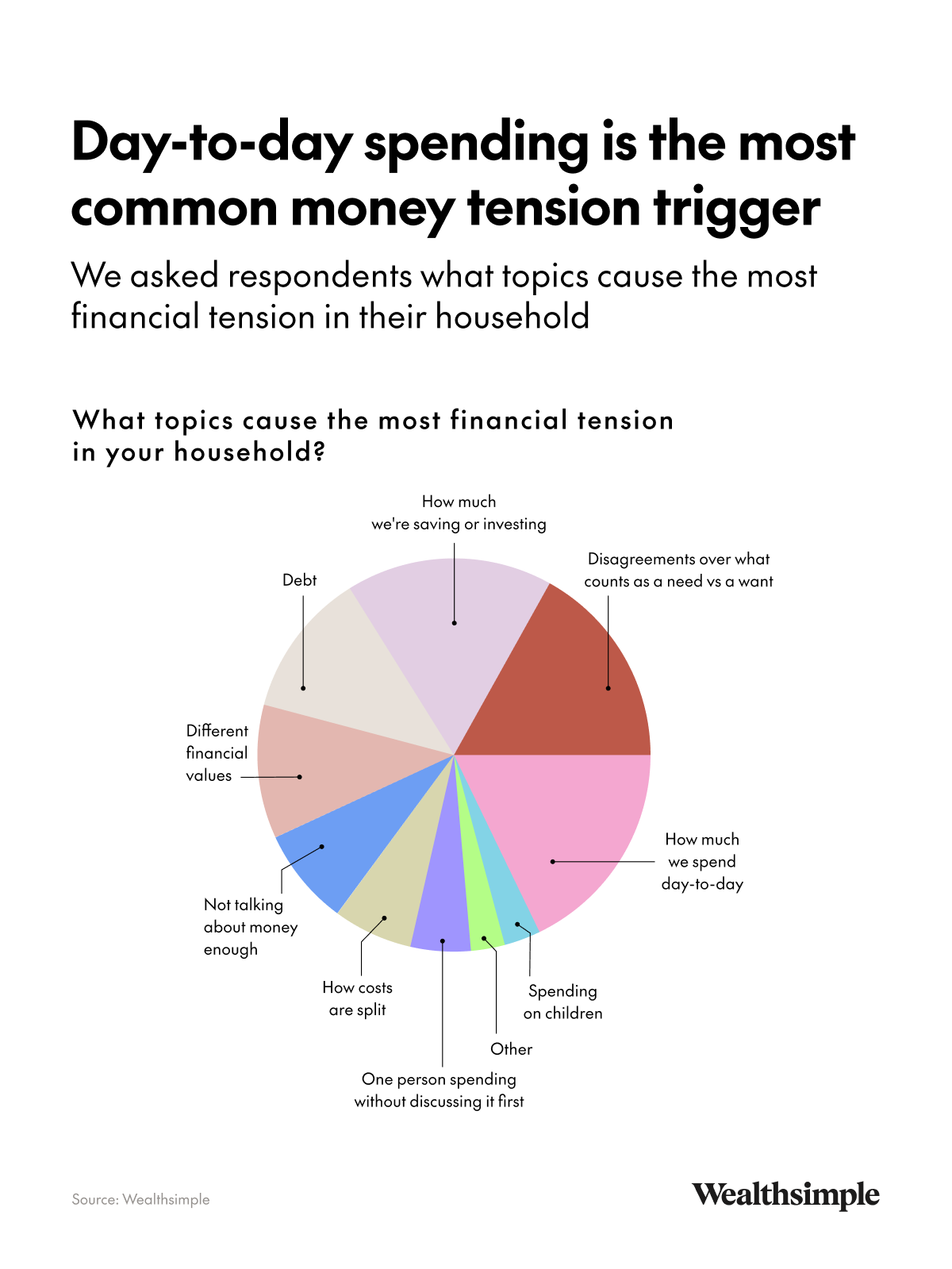

Major purchases aren’t the biggest source of money conflict

You might expect financial tension to mostly rear its head whenever a household buys a car, a home, or another significant purchase. We found the opposite. Groceries and subscriptions were the top source of household financial conflict for 32% of respondents, with another 29% pointing to disagreements over whether a purchase qualifies as a "need" rather than a "want." The least common source, interestingly, was child-related expenses — a sign many parents, even those in acute financial stress, want the very best for their children.

But the nature of household spending among our respondents also opens the door to miscommunication. We found most couples either have one person make all day-to-day spending decisions, or each person will have full responsibility for a different expense (groceries versus laundry, for instance). This dynamic sometimes leads to resentment or avoidance rather than open discussion. One respondent told us they pay for most of their children's activities and clothes alone because bringing up the issue of spending with their partner is too difficult.

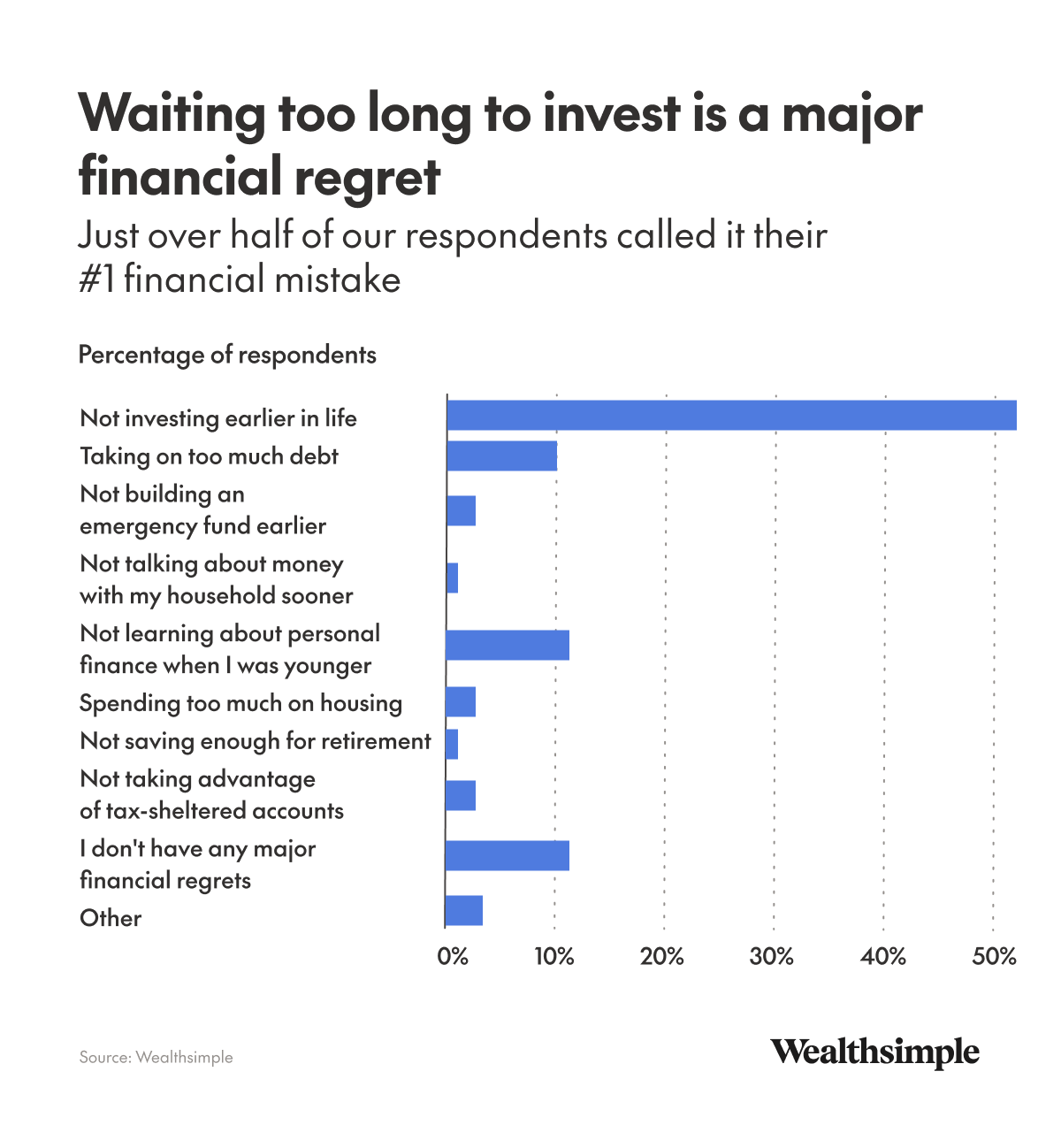

Most households wish they invested earlier

By far, Canadian households recognize the importance of investing to a stable financial future. More than half of respondents told us their single biggest financial regret was not investing sooner, while nearly 70% wished they’d been taught how to build wealth earlier in life.

But a lack of financial education isn’t the most common reason households don’t invest — inadequate income is. And this isn’t just a problem for non-investors. About half of respondents also told us they’ve cut back on a variety of expenses, including both investing and discretionary spending, over the past year. Most of them blamed the rising cost of housing.

The data also tells a more hopeful story

In spite of the sacrifices they’ve made over the past year, Canadian households we spoke to are largely weathering the current financial storm. Two-thirds said they'd reach for emergency savings to help cover a surprise $5,000 expense and a slim majority described their family’s current situation as “comfortable” or “strong.”

Canadians are also very optimistic about tomorrow. 70% said they were either “somewhat confident” or “very confident” in their family’s financial future and, although many households’ operating budgets are under strain, the vast majority continue to invest, one of the best ways to build long-term financial wealth.